California Home Ownership Act: $25 Billion Plan to Help Middle-Class Buyers Explained

The question California voters are facing

For millions of Californians, "Is owning a home here a dream that's out of reach?" is not a rhetorical question. It's the math of a paycheck against a median-priced home, a savings account against a down payment, and a credit score against a mortgage rate. The state's affordability crisis is one of the most stubborn problems in the country, and a new ballot measure is asking voters to do something concrete about it.

The proponents frame the problem simply. The classic American dream of owning a home is slipping away from working and middle-class families, the people they describe as the backbone of the state. The proposal in front of voters is a structured response to that gap.

What the measure actually is

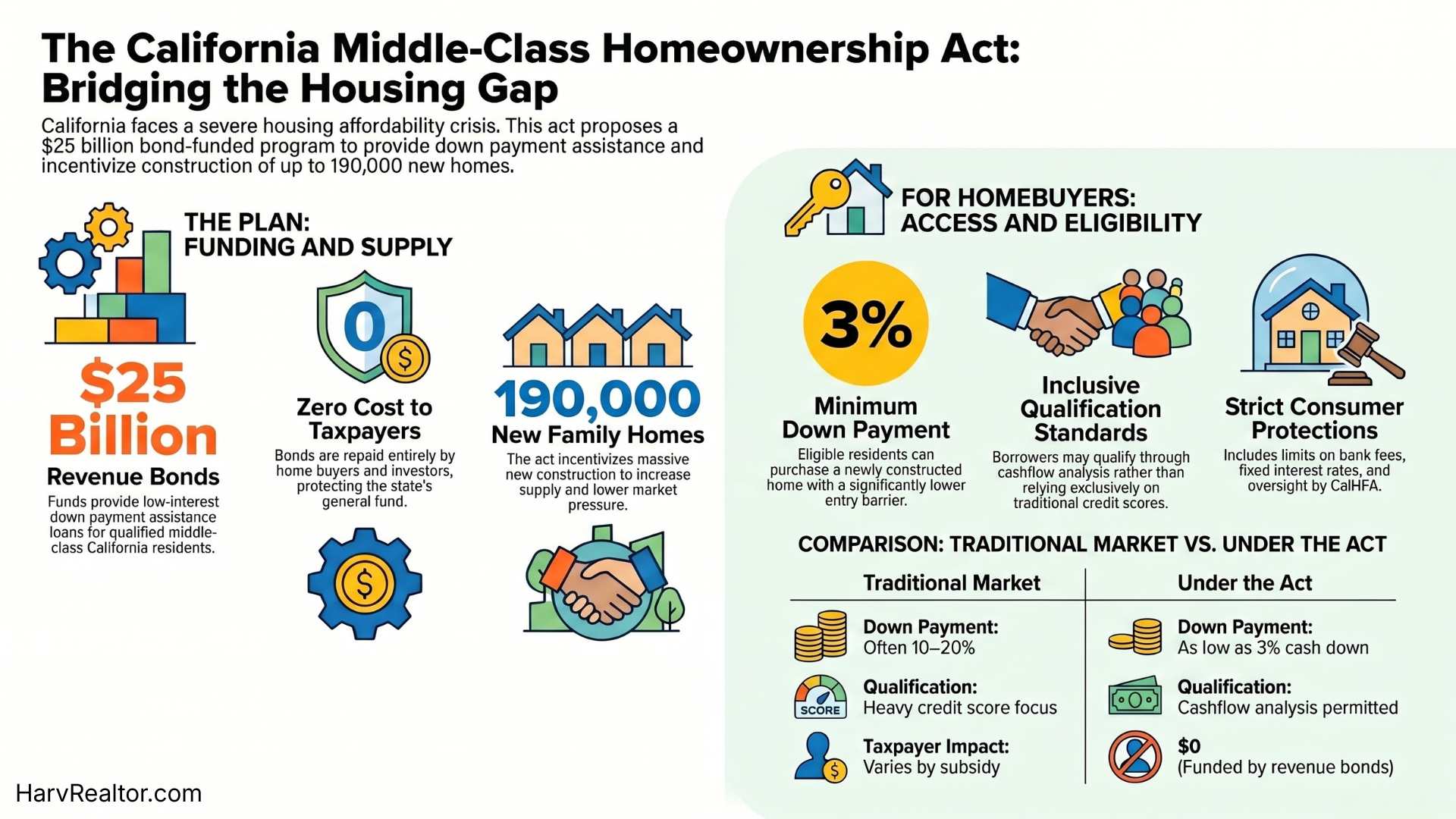

The official name is the California Middle Class Home Ownership and Family Home Construction Act. It would authorize the state to issue $25 billion in bonds to fund down payment assistance loans for buyers of newly constructed homes. The emphasis on new construction is intentional. The goal is not just to help individual buyers, but to use that demand to spur new single-family home building.

Key distinction: the assistance is targeted at newly built homes, not resale inventory. That single design choice shapes the rest of the program, from who benefits to how it's supposed to ease the broader housing shortage.

How $25 billion in aid works without new taxes

The whole plan is built around one big number, $25 billion, that the measure would authorize for down payment assistance loans. The natural question is, where does that money come from. The answer, according to the measure, is not new taxes. It is funded by what are called revenue bonds.

The easiest way to think about a revenue bond is this. Investors buy the bonds. The state lends that money out as down payment assistance. The home buyers who receive the loans repay them over many years, and that stream of repayments is what pays the bondholders back. The proponents describe the program as designed to be at no cost to taxpayers, because the home buyers themselves, not the general fund, are the ones paying back the bonds.

That mechanic is the same playbook used by Cal HFA and other public housing finance agencies. What is unusual here is the scale.

Who qualifies

The qualifying path is laid out clearly in the measure. The biggest news inside the eligibility list is the cash flow analysis option, which expands access well beyond the traditional credit-score-only model.

- California residency. You must be a California resident.

- Primary residence required. The home you buy with the assistance must be your primary residence. You have to actually live in it.

- 3% minimum cash down payment. You bring at least 3% of the purchase price in cash to the table.

- Demonstrated ability to make monthly payments. The standard underwriting question, can you afford the loan.

- Cash flow analysis as a qualifying path. Lenders can look beyond the traditional credit score and use your cash flow to qualify you. This is the door that opens access for many self-employed and non-W-2 buyers who are creditworthy in practice but underserved by credit-bureau scoring.

- Repayment on sale or refinance. The down payment assistance loan is repaid when the home is sold or refinanced, alongside ongoing monthly payments while you live there.

The goal: roughly 190,000 new homes

The supporters of the measure project that it will help spark the construction of approximately 190,000 new homes across the state. That's the big aggregate number. The CA Homes Coalition site, in a separate framing, has cited a 100,000 to 150,000 home range, so the exact projection depends on which proponent document you're reading. Either way, it's housing supply at a scale California hasn't added in a generation.

Behind the headline number are four stated goals.

Who is backing it and why

The coalition behind the measure is broader than the typical single-interest backing. It includes organized labor, the real estate industry, and former state legislative leadership. Each comes at the same problem from a different angle.

"The home affordability crisis has put homeownership out of reach for too many working families."

That's Pete Rodriguez, Second General Vice President, United Brotherhood of Carpenters and Joiners of America. For organized labor, this is positioned as both a homeownership package and a construction-jobs package.

"This measure addresses California's housing shortage and affordability crisis, creating pathways to homeownership."

That's Tamara Suminski, 2026 President, California Association of REALTORS®. The measure was introduced by former California Assembly Speaker and Senate Majority Leader Bob Hertzberg. The framing across all three voices is consistent: this is positioned as a jobs-and-homeownership package, not just a buyer subsidy.

Consumer protections

Any large-scale public lending program raises questions about cost, fees, and accountability. The measure addresses those directly with a list of consumer-protection provisions.

- Administered by Cal HFA, the California Housing Finance Agency, the state's existing housing-finance authority.

- Fixed low interest rates on the down payment assistance loans, set under Cal HFA standards.

- Strict limits on bank fees, with disclosure requirements built into the measure.

- No prepayment penalties. Borrowers can pay off their loan early without being charged.

- Annual independent audits, so the program's financial performance is reviewed by an outside auditor every year.

What happens next

The California Association of REALTORS® has confirmed the measure has qualified for the November ballot. From here, the path is straightforward. Voters will see the measure on their ballot, the campaigns on both sides will make their case, and Californians will decide whether the state authorizes the bonds and stands up the program.

Whatever you think about the measure on the merits, the question it forces is direct. Is a $25 billion, Cal HFA-administered, no-new-taxes-claimed down payment program the right tool to unlock middle-class homeownership in California? That's the question voters will answer.

Key facts at a glance

Sources

- California Association of REALTORS®: [car.org/aboutus/mediacenter/news/homeownershipact](https://www.car.org/aboutus/mediacenter/news/homeownershipact)

- CA Homes Coalition (proponent site): [cahomescoalition.com](https://www.cahomescoalition.com/)

- California Secretary of State (verify ballot text and timing): [sos.ca.gov](https://www.sos.ca.gov/)

Watch the video

Disclaimer

This content is informational and not legal or financial advice. Always verify ballot details with the California Secretary of State and consult a qualified professional before making real estate decisions.

Talk it through

If you're weighing a buy, sell, or refinance decision in Fremont, San Jose, Milpitas, Newark, Hayward, Union City, or anywhere across the East and South Bay, I can walk you through how a measure like this could change your numbers, your timing, and your options.

Your Local Real Estate Team

Harv Balu

REALTOR® | GRI, CIPS, PSA, FTBS · REALTY EXPERTS®

CA DRE# 02195792

REALTY EXPERTS® · 41051 Mission Blvd, Fremont, CA 94539