The Overpricing Trap: How to Price Your Fremont Home to Sell (Without Costing Yourself Six Figures)

Price your home $50,000 too high, and it does not cost you $50,000. It can cost you six figures. That sounds backwards, so stick with me. Once you see the mechanics, you will never look at "list high and come down later" the same way again, and you will see why a smart Fremont home pricing strategy starts with knowing how to price your home to sell, not how high you can list it.

"List high, we can always come down" feels safe. It is the costliest mistake.

It is the most natural instinct in the world. You worked hard for this home, the market has been strong, so why not aim above where the comparable sales land and leave room to negotiate? Worst case, you drop the price later. No harm done.

Except there is harm, and it stacks up quietly while your home sits. Overpricing does not give you a cushion. It hands your leverage to the buyer, one week at a time. As a NAR Pricing Strategy Advisor (PSA), I spend a lot of time on the why behind a list price, and the why matters more here than almost anywhere else in the sale.

The pricing pyramid: why market value reaches the most buyers

Real estate has a simple model for this called the pricing pyramid, and it explains the whole trap in one picture. Price your home right at market value and you sit at the wide base of the pyramid, where the largest pool of ready, qualified buyers is looking. Price above market and you climb toward the narrow tip, where far fewer buyers are searching and even fewer believe the number. Price a touch under market and you widen the pool even further, which is how competition and multiple offers get started.

The goal is not to give the home away. It is to land where the most buyers are actually looking, so the most people see it during that first, high-attention window. That is exactly why correctly priced Tri-City homes have been clearing so fast, and often above asking, as the local numbers further down show.

Your first one to two weeks are the prize. Overpricing burns them.

When your home hits the market, it gets more attention in the first week than at any other point in the sale. The serious, pre-qualified buyers in your area have alerts set. They have been watching for weeks or months. The instant a new listing in their price range and target area goes live, they get the ping, and they move. The first one to two weeks bring your most showings and your most motivated buyers.

Price it where the market actually is, and those buyers show up, tour, and compete. Price it above the market, and they do the math in two seconds, decide it is not for them, and keep scrolling. You do not get that audience back. The spotlight moves on to the next new listing, and your home gets skipped while it is still the newest thing on the market.

Days pile up, and the story flips against you.

This is the part most sellers do not see coming. Buyers and their agents watch days on market like a stock ticker. A home that has been listed for a day reads as "get there fast." A home that has been listed for forty days reads as "what is wrong with it?" or "that seller must be motivated by now."

Nothing about your home changed. The roof is the same, the kitchen is the same, the location is the same. But the story the market tells about your home shifts, and not in your favor. Every week your listing lingers, negotiating leverage slides a little further from you and toward the buyer. By the time an offer comes in, it is built around your weakness, not your home's strengths.

The price-cut spiral: chasing the market down.

So you cut the price. Reasonable move. But a single reduction rarely fixes an overpriced listing, because the original number already told the market you were testing it. One cut signals you are willing to move. Often it is not enough, so a second cut follows.

Now you are chasing the market down instead of leading it. Each reduction is a fresh signal of weakness, and buyers wait to see if another one is coming before they bother to write. You set out to lead the conversation and ended up reacting to it.

It sells. Just under market.

Eventually it sells, because almost anything sells once the price meets the market. The problem is which number. After the lost prime window, the extra weeks of mortgage payments, taxes, and insurance you carried, and the eroded leverage, that home often closes below what it would have fetched if it had been priced right on day one. As the example below shows, a $50,000 stretch at the top can turn into roughly a six-figure loss by the end. The "cushion" was never a cushion. It was money draining out a week at a time.

An illustration of how the math turns

This is an illustrative example, not a prediction or a guarantee of any result. Picture a Fremont or Mission San Jose tier home with a true market value around $1.49M. Drag the slider below to list it above market and watch the trap unfold.

See what overpricing actually costs

Drag the slider to list this example $1.49M home above its true market value, and watch the trap unfold. The higher you reach, the longer it sits, the more you cut, and the lower it finally sells.

About $75K left on the table at sale, plus roughly $17K in extra carrying costs while it sat.

Illustrative model for a $1.49M-tier home, built to show the mechanics of the overpricing trap. It is not a prediction, a guarantee, or a valuation of any specific property. Your actual days on market, reductions, and sale price depend on your home, your pricing, and current market conditions. Let me build you a real pricing strategy from live comps.

The takeaway: in this illustration, listing about $85,000 over market turns a fast, at-asking sale into a 67 day slog with two price cuts and a final price well under market, roughly a six figure swing on a single pricing decision.

In the example above, the overpriced version lists at $1,575,000, takes two reductions of $50,000 each, and finally closes around $1,415,000 near day 67. The correctly priced comparable sells in about 9 days at roughly 99% of list. Same house, same market. The only thing that changed was the opening number.

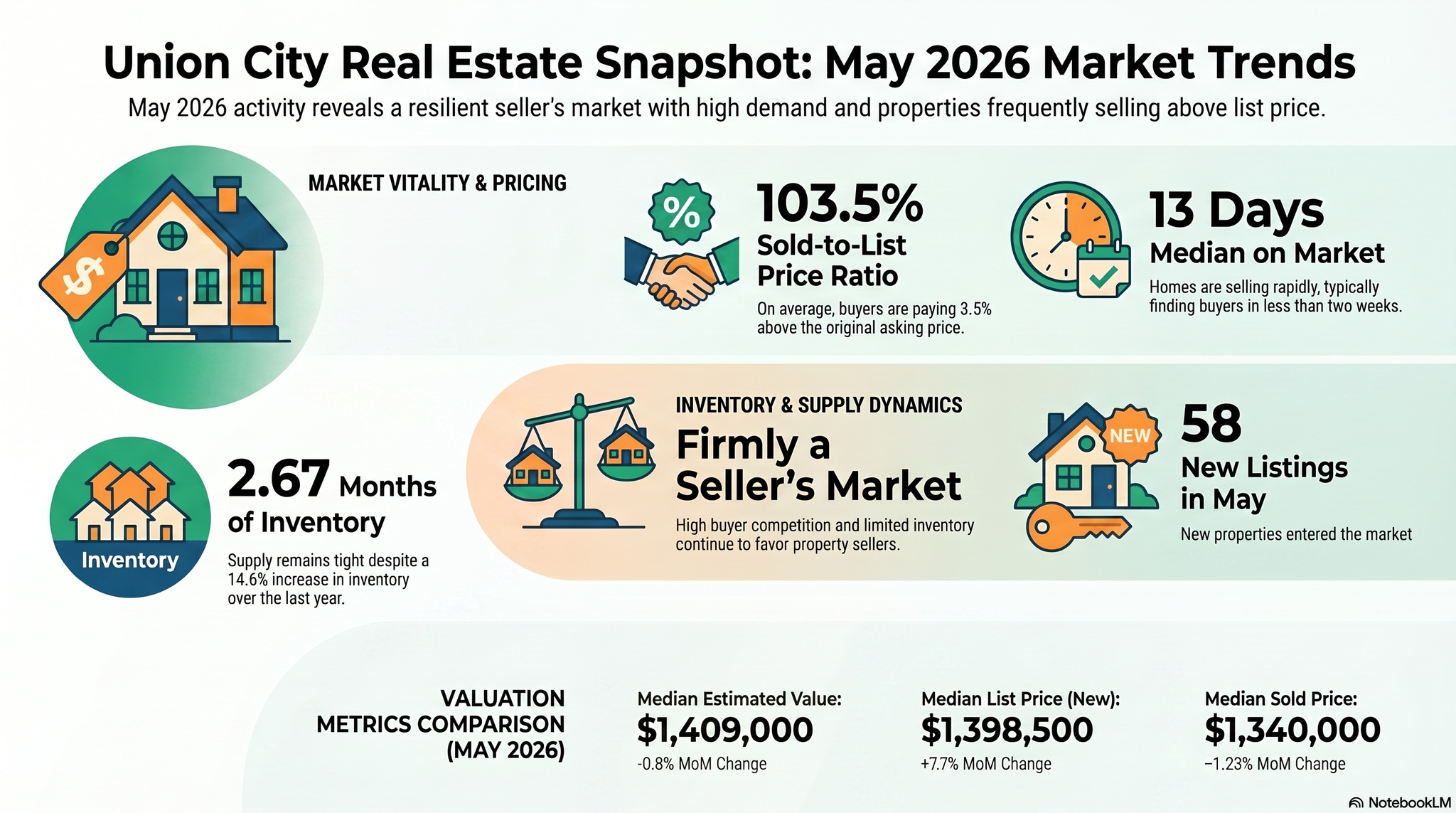

The local data backs this up.

This is not theory in our market. Correctly priced Tri-City homes have been selling fast and above asking, which is exactly the momentum overpricing forfeits.

Sellers who priced correctly were not leaving money on the table by listing at market. They were getting bid above it, quickly, because the price invited competition instead of suspicion. This applies anywhere, and in our market the data shows the upside is real. The same logic holds in the Central Valley, in Manteca and Stockton, even though the price points and pace differ.

Buyers, this is for you too.

If you are buying, an overpriced listing is your problem as much as the seller's. Pay over the comparable sales and your lender's appraisal may come in low, leaving an appraisal gap you have to cover in cash or renegotiate around.

Overpaying in a hot moment can also leave you underwater if you need to sell sooner than planned. A pricing-savvy agent reads the comps, spots when a list price is detached from reality, and structures your offer so you compete hard without overpaying. That protects your money on the way in.

How to price it right the first time.

Pricing is a strategy, not a guess. This is the actual work behind a list price.

The fastest way to start is a real CMA on your own home. You can request a free home valuation to see roughly where your number should land, and then we refine it together from live comps.

Do this well and the dynamic flips. Instead of you chasing buyers down with cuts, the right buyers come to you, competition builds, and offers land at or above asking. That is what pricing strategy actually buys you.

Want to see what is currently active in your neighborhood before you decide? You can browse live listings anytime at HarvRealtor.com.

Harv Balu, REALTOR®, PSA

Disclosures

Market figures cited here are from Bay East and bridgeMLS via RPR and Altos Research for Fremont and Union City, May/June 2026, as reported in Harv's market reports linked above. The dollar pricing example is illustrative only and is not a prediction or guarantee of results in any specific transaction. All data is deemed reliable but not guaranteed and is subject to change. Equal Housing Opportunity.

Frequently asked questions about pricing your Fremont home

What happens if you overprice your house?

Overpricing usually costs you more than it makes you. Buyers filter their searches by price, so listing above what the market supports hides your home from the very people who would pay full value, and the listing sits, goes stale, and draws lower offers than a right-priced home would. In this Tri-City market, correctly priced Fremont homes have recently sold at a median of 104% of list in about 11 days, so overpricing means giving up that early momentum (see the Fremont market report linked in this post).

How do I price my home to sell in Fremont?

Start with real comparable sales, not a number you wish were true. A REALTOR runs a Comparative Market Analysis on homes near yours, similar in size, age, and condition, that closed recently, and prices your home to compete with them. Pricing at or slightly under true market value is what triggers strong first-week interest and, in a tight market like Fremont or Mission San Jose, multiple offers. As a NAR Pricing Strategy Advisor (PSA), that is the exact analysis I build for every seller I represent.

Should I price my home high to leave room to negotiate?

This is the most expensive myth in home selling. Serious buyers and their agents research comparable sales before they ever tour, so a high price does not invite negotiation, it invites them to skip your home. The buyers who do come expect a discount, so you negotiate down from a number that scared everyone else off. Pricing right to market draws more buyers at once, and competition, not a padded list price, is what actually pushes your final number up.

How much does overpricing a home cost you?

It costs you twice, in time and in dollars. Every extra week on the market is another mortgage payment, more taxes, and more carrying costs coming out of your pocket. Worse, a home that lingers signals to buyers that something is wrong, so the eventual sale price often lands below what a well priced home would have fetched from the start. The longer a listing sits, the more leverage shifts to the buyer, and that shows up in your bottom line.

How long should a house be on the market before you lower the price?

Watch the activity, not just the calendar. If you have had plenty of showings but no offers, your price is close but not compelling, and if you are getting very few showings at all, buyers are screening you out on price before they walk in. Either signal in the first couple of weeks means it is time to act, because your strongest window of buyer attention is right at the start. Waiting too long only forces deeper cuts later.

Why isn't my house selling in Fremont?

Nine times out of ten it comes down to price, condition, or how the home is presented, and price is the one that overrides everything else. A home that is not compelling on price will not sell no matter how good the photos are, because buyers compare you side by side with everything else in their range. Before you assume the market is the problem, look honestly at how your list price stacks up against recent nearby sales. That comparison usually tells the whole story.

Does an overpriced home affect the appraisal?

Yes, and this is where an inflated price can kill a deal. An appraiser values your home on comparable sales and condition, not on your asking price, so even a buyer willing to overpay can hit an appraisal gap their lender will not finance. That forces the buyer to bring extra cash, renegotiate, or walk. Pricing to true market value from the start keeps your appraisal, your contract, and your closing all pointing at the same number.

Harv Balu

REALTOR® | GRI, CIPS, PSA, FTBS · REALTY EXPERTS®

CA DRE# 02195792